Year one of the Tech Decade in Banking will bring no shortage of tension between technology investments and earnings targets.

Well GonzoBankers, the gang is back to work and we are all headed face-first into 2020 – a year with more uncertainty than most about how things will turn out. So, to get your Gonzo executive brains warmed up for a new year, I offer you 20 important banking realities for 2020 to guide your strategic execution efforts:

1. We are entering the “tech decade” in banking. In the years 2010-2020, new tech adoption transformed customer expectations. The next decade will see tech significantly disrupting bank shareholder value. Wells Fargo analyst Mike Mayo got a great deal of attention this year when he claimed that the coming decade will be “the biggest tech transformation in the history of banking.” For execs who climbed the ladder in finance, lending or branches, buckle in because the techies are about to steal the show.

2. Banks are most afraid of big tech, just when these players face regulation. In the soon to be released What’s Going On In Banking study, Cornerstone’s Ron Shevlin shows that both bank and credit union execs are most fearful of big tech (Amazon Prime, Venmo, Apple Card) primarily because of their great data reach and ability to drive customer experience. However, between anti-trust regulations, algorithm investigations and states focused on privacy (e.g., California CCPA), it’s hard to imagine just how far techies will be able to upend the nuts and bolts of the banking industry.

3. Community banks and credit unions do not fear each other. While these independents all give Lake Wobegon nods to themselves, they view their own peers as lacking the scale and tech to remain competitive. Here’s a great question for community bank executives: What would it take for your local competitors to fear you as much as a Top 5 player?

4. Slowing revenue growth will spur serious internal politics at banks. Chief financial officers have been warning about plateauing net interest income for more than a year, and the reality has finally hit 2020 budget forecasts. Watch your backs, executives – your peers may be in the chief executive officer’s office right now saying they have “concerns” about your division. GonzoBankers will need to figure out how to keep transforming their businesses when discretionary dollars are scarce.

5. Consolidation will continue in the middle of the industry. Slowing revenue will mean many executives turn to taking out costs through mergers and acquisitions (M&A). 2019 was a sneak peak of many larger mid-size deals (TCF/Chemical, First Horizon/Iberia). Merger of equals discussions will continue to create larger mid-size banks in the $10 billion to $100 billion asset range.

6. New regional banks will struggle with operational maturity and customer experience. M&A is causing many banks to grow so quickly that the “chassis” of the organizations may start to crack. While the whizzes in finance and credit can scale fast, the worlds of operations, information technology (IT) and digital cannot. Operationally, these M&A-birthed regionals are a mess that will require years of process improvement and streamlined automation to achieve the customer experience levels necessary to stay independent.

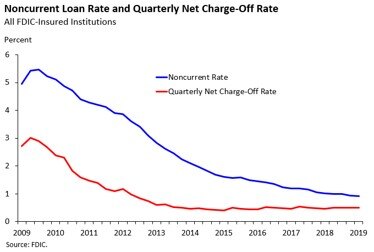

7. Banks are high on the “opiate” of zero credit costs … be careful. Delinquencies and charge-offs have been so low that many fast-growing banks have put near nothing into provision given Allowance for Loan and Lease Losses (ALLL) levels. It’s been a nice ride. Unfortunately, these tiny credit loss levels seem to overstate earnings psychologically. Take a step back and remember what even normalized provision might do to earnings.

8. No bank has taken a sharp enough pencil to branches. With robust deposit growth in the past decade, banks have kept an eye on staffing and watched their average deposits per branch grow nicely. The issue? There are still 106,000 branches when credit unions are considered, and banks are overestimating the contribution many branches are making to retaining and growing revenue, all while starving investments in marketing, digital and data maturity.

9. Most banks can’t downsize branches because of anemic digital growth capabilities. We are in the infant stages of integrating digital marketing and online origination. Today, most institutions generate fewer than 5% of deposit accounts online. This must change from the top. The number of monthly loan closings and deposit accounts should be reported to the CEO and board each month on a poster board in red until these paltry levels spur commitment, action and growth.

10. Mobile adoption is maturing, but the mobile banking experience is still at ground zero. Mobile banking penetration stands at roughly 55% of smartphone users, but most of these users are not active with features like alerts, peer to peer (P2P) payments, card controls, account opening and digital service requests that will solidify the experience and bring real efficiencies to the business model. These gaps exist today because banks have a hell of a time trying to build and integrate these capabilities with a crazy quilt of industry vendors. The only solution is to keep executing on a formal roadmap of improvements and build internal integration, user experience and data skills that will act as the “glue” in a world full of imperfection.

11. The death by 1,000 cuts in payments continues … with little transparency to executives. Whether it’s Amazon Prime Cards, Venmo, Apple Card, Real-Time Payments or P2P, bankers will continually see severe pressures on interchange revenue. Bank executives need to be more exposed to data on growth/margin trends in their payments businesses and develop action plans to improve revenue. In most cases, this information is buried three levels down.

12. Digital lenders are out-designing and out-executing banks and credit unions. Experian recently reported that fintechs doubled their market share in four years and are now generating half of all unsecured loans to consumers. Bankers keep scratching their heads and saying, “How can they make it so simple?” It’s time to steal their playbook – quickly!

13. Commercial banking is still insulated from disruption, but it’s time to shake up the model. Today, there’s little evidence that fintech micro-business lenders are eating into the bread and butter of the $1 million to $20 million commercial loan market that community and regional banks dominate. However, these businesses are increasingly run by next-generation managers who want a more digital customer experience. Improved mobile banking and e-payment offerings for business clients and the digitization of commercial lending must become top priorities for commercial executives. The delay has been too long.

14. The fintech bubble will lose air soon – but this could be an opportunity. Plaid’s unicorn sale to Visa for $5 billion and 35 times revenue and Chime’s one-year quadrupling of valuation to $5.8 billion may prove to be the bellweather events when fintech multiples peaked. The good news is that future valuation declines and newfound humility may allow fintechs to really roll up their sleeves with banks on transforming the industry without the techies constantly daydreaming a nice “exit strategy.”

15. Major industry IT vendors will face brutal “political” pressure from banks. Fair or not, banks are building more collective steam against an oligopoly of vendors like FIS, Fiserv and Jack Henry, which have enjoyed rising profits and stocks while decreasing customer loyalty. With the American Bankers Association and state banking leagues making this a top agenda item, bank CEOs will be more open to taking risk on alternatives to the Big 3 vendors.

16. Huge data investments are still being met with tiny ROIs. There have been hundreds of warehouses “spun up” and data lakes flooded, but most banks are still running their businesses the old-fashioned way. CEOs need to force a change. Simple task: Require every executive to outline the top three questions they cannot answer today that analytics could help solve. Build the list, prioritize and execute.

17. Robotic process automation and artificial intelligence will be big winners, but they are nowhere at most banks. Cornerstone research reflects that only 6% of banks have already deployed RPA and only 4% are using AI to date. For all the talk, it’s time to focus on pragmatic pilots and execution.

18. The talent arms race is beginning to cut into progress on operating efficiency. With 3.5% unemployment in the United States, labor costs increased at their fastest pace in a decade during Q4 2019. In working to attract talent in digital, marketing, IT and risk, banks need to have rigorous processes to get the right candidates. The risk of overpaying for mediocrity right now is huge.

19. Banks need to elevate their chief information security officer (CISO) role and beef up security talent … NOW! There’s a vibe out there today that the bad guys are getting more organized, relentless and adaptable than ever before. Information security priorities have nothing to do with compliance and everything to do with protecting the reputation and liquidity of big balance sheets worth a lot of money. Too many institutions are turning down the small six-figure investments needed to address this risk. In these scary times, don’t be penny wise, pound foolish.

20. Banking organizations remain over-managed and under-led. In Cornerstone’s efficiency studies, we regularly see average management spans of controls to be only three to five employees and bank compensation top-heavy among managers versus the actual doers. Automation, self-service and data analytics will allow banks to whack out management costs in the future and retain only value-adding leaders – those creative builders with ideas about the future who can drive commitment and outcomes.

In our first year of the tech decade in banking, there will be great tension between the investments required to transform the business and the tough realities of 2020 earnings targets. GonzoBankers will do their best to “thread the needle” between these two forces and make gritty progress during a pretty wild time.