Banks and credit unions are facing a worrisome paradox today: Keeping up with technological advancements has become more critical, just as the vendor outsourcing market has become more fragmented, cumbersome, and less service-oriented.

The majority of banks and credit unions that outsource their core processing to major core vendors are putting the future of their enterprise technology in the hands of vendors that rely much less on core systems to drive their revenue and stock valuation.

Revenue speaks loudly to vendors in terms of which products attract the beefiest R&D budgets and where the vendors’ top talent is deployed. Here are a few key observations:

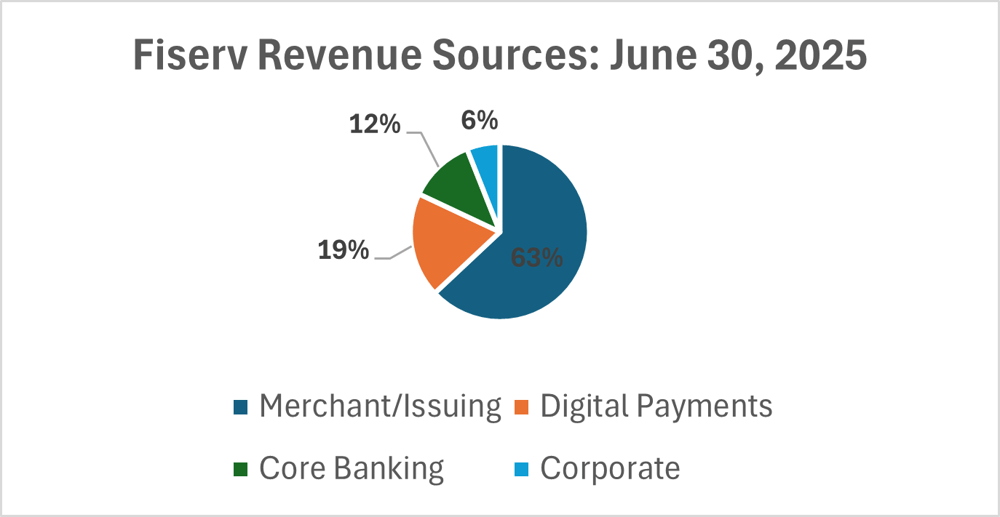

Core processing is a tiny 12% of Fiserv’s revenue as of 2Q25, and core revenue is down 17% since 2Q21. Fiserv is primarily a cards/merchant/payments operation now.

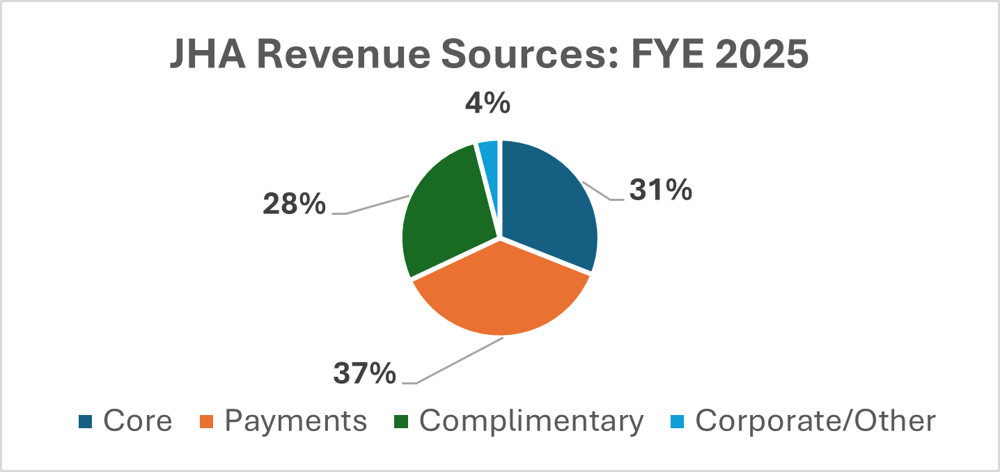

Less than one-third of Jack Henry’s revenue is derived from core banking services as of its FYE 2025, and core is the company’s lowest growth segment since 2021.

FIS does not report revenue in terms that can differentiate among cards, payments, merchant, and core revenue. That said, the firm’s major acquisition and sale of Worldpay, with the simultaneous purchase of the TSYS issuer business, underscores the company’s strong focus on payments vs. regional and community banking core services.

As the relative share of core processing revenue shrinks, service and support also seem to be slipping, and there’s no easy answer to address these challenges. In Cornerstone’s discussions with hundreds of financial institutions, bankers lament that these large technology companies have lost many of the knowledgeable and gritty professionals who delivered detailed configuration support, integration assistance, and custom development needs in the past. Results of surveys from major trade associations like the American Bankers Association emphasize this message. Rather than technology factors, the top reasons ABA found for banks contemplating a conversion to a new system were customer service (42%) and the overall relationship with their core provider (38%).

Vendor service perceptions have also been amplified by a key trend over the past decade. Most new core deals are now outsourced, and very few banks and credit unions migrate core from outsourced to in-house anymore. While outsourcing makes business sense in today’s world, a challenge arises when clients need custom work done regarding products, interfaces, and new fintech partnerships; the pace of addressing these needs can be painstaking.

To add to the confusion, most vendors have announced core framework modernization strategies involving various combinations of legacy core systems with plug-and-play microservices and applets for added functionality and advanced data management.

Here’s the issue: If bankers are already experiencing service challenges, it becomes a leap of faith for them to buy into a modernization journey with core vendors needing to deliver stellar performance in these “Critical 5” areas:

-

System integration—third-party and internal

-

Accountability and communications in projects involving multiple vendors, including competitors

-

Robust API and enterprise integration layer development and sensible pricing for it

-

New cloud-native application development

-

Data management across a complex application stack

Clearly, most bankers do not feel this list represents a skill set that outsourcers can nail in their sleep. This is a new world of technology for their teams as well.

Success or failure in core modernization will be measured at the front line, as bankers battle-test the effectiveness of vendor deployments.

-

Do the applets work?

-

Will the core vendors truly work with ancillary system partners that are also competitors?

-

Can they/how will they create and manage a tech environment involving multiple system integrations and data from disparate systems?

Until they can do that, bankers will find themselves instinctively reaching out to hit Play on Weezer’s “Hash Pipe” when reading about their core vendors’ modernization promises.

Bottom line: Navigating this new vendor environment will require a particular mindset that challenges the way banks and credit unions evaluate their core providers and what those providers’ roles should be. Here are a few things for bankers and credit union executives to take into consideration as their major vendors work through the modernization tap dance:

-

Start with the most important question: Has the modernization strategy proposed by my core vendor been successfully implemented by any core vendor?

-

Add in-house core system delivery into your future potential scenarios. If you’re outsourced, you’ll likely stay that way for the redundancy/DR and security benefits. We get it. But seriously. If your institution believes it can perform all or some of the Critical 5 tasks better than your vendor—especially data management and integration—an in-house environment might be worth a look. It really comes down to how much the financial institution trusts its vendor to deliver on the Critical 5 capabilities.

-

Review the market for boutique integration service providers who are building enterprise integration layers and execution experience around the major cores. Activity and interest have been very vibrant around firms such as PortX, Kinective, nCino (Sandbox), Trabian, Savana, and Coast. Banks and credit unions are exploring if they can become more self-reliant on integration with partnerships like this.

-

This market is ripe for the reemergence of co-ops and standalone bank service centers that are like credit union service organizations (CUSOs). Delivering Big 3 vendor functionality in an independent and accountable service center would surely evoke industry attention.

-

The Big 3 aren’t the only core providers out there. They do a lot right, and banks and credit unions should consider them in their planning. However, niche and regional players are working to demonstrate a service advantage over the Big 3 while maturing their own modern technology chops. Depending on your asset size and complexity, they are worth a close, close look.

The point here is not to beat up vendors working to turn the “battleships” of legacy core systems and move into the modernized technology world. The market will take care of that as needed.

Most banks want their vendors to succeed in their modernization efforts. The ABA reports that 69% of banks are somewhat or extremely likely to remain with their existing cores. Yet, this drastic change in both technology and the revenue models of major outsourcers means that banks and credit unions must rigorously “trust but verify” their vendors’ modernization commitments while seeking ways to become more self-reliant in the Critical 5 areas of managing the new modern tech stack.

Scott Hodgins is a senior director at Cornerstone Advisors. Follow Scott on LinkedIn and X. Steve Williams is chief executive officer and a founder partner at Cornerstone Advisors. Tune in to Steve’s Plugged In podcast and follow him on LinkedIn and X.