What community financial institutions may overlook as they begin to scale AI

There’s no shortage of content outlining how AI will transform banking: faster decisions, lower costs, improved experiences, smarter growth strategies… Spend five minutes with a vendor or at a conference and you’ll hear some version of this theme.

To be fair, most of it is directionally right. But almost all of that conversation is focused on what AI will enable. Very little is focused on what it might quietly reshape. And not necessarily through failure or misuse, but through normal, successful adoption.

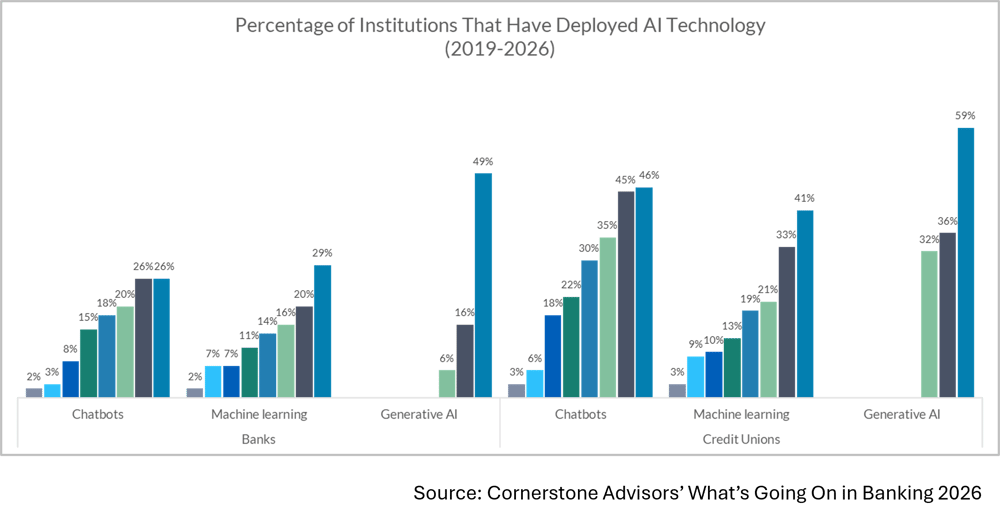

Adoption is growing. Cornerstone’s 2026 What’s Going On in Banking report illustrates this point, as AI technology adoption, particularly Generative AI, continues to accelerate for both banks and credit unions.

If you look back, every major shift in banking came with second-order effects that didn’t show up in the pitch deck. Core systems improved efficiency but concentrated dependency. Digital channels expanded access but fragmented relationships across channels and touchpoints. Digital account opening accelerated growth and invited synthetic fraud at scale.

AI is likely to follow that same pattern.

For most community banks and credit unions, the question right now isn’t whether AI works. It’s where it fits, how to use it, and how to get started. That’s exactly why this moment matters. Because the blind spots don’t show up after full adoption; they start forming early, while everything still looks like progress.

Here are three to keep an eye on.

1. The Transparency Gap

As AI becomes embedded in decision making, institutions will increasingly rely on systems that are difficult to fully interpret. This isn’t new. Banks and credit unions have always used third-party models and vendor platforms. But AI introduces a different level of complexity. Models will become more dynamic, data inputs broader, and outputs more probabilistic than deterministic.

Over time, this creates a subtle but important shift where institutions will still own and be accountable for the decisions but increasingly rely on externally defined logic to make them. That distinction sounds small, but it’s not.

The Apple Card situation was an early signal. Regulators didn’t find illegal discrimination, but the issue escalated anyway because customers and eventually regulators couldn’t clearly understand how decisions were made. The problem wasn’t just the outcome, it was the inability to explain it in a way that made sense.

As models become more complex, the gap between performance and explainability will widen. And in the regulated, trust-based industry of banking, that gap doesn’t stay theoretical for long.

This isn’t a reason to slow down AI adoption, but it is a reminder that decision ownership doesn’t disappear just because decision logic moves somewhere else.

To control the transparency gap, be intentional about:

- Making sure critical decisions can still be clearly explained — not just internally, but externally as well

- Understanding how outputs are produced — not just whether they perform well

- Avoiding a future where too much decision logic sits inside a single vendor or system

2. The Slow Death of Institutional Knowledge

AI will make it easier for institutions to produce consistent outcomes. That’s one of its biggest advantages. But it will also start to change how expertise is built and retained across the organization.

This shift won’t come from everyone using their shiny new Copilot license directly. It will come from AI being embedded into systems, workflows, and decisioning processes. Over time, work will become more structured, more guided, and more consistent. This is certainly a benefit, but it also may come with a trade-off.

Institutional knowledge has never come from following a process “to a T”. It comes from understanding when the process doesn’t apply, handling edge cases, making judgment calls, and working through situations that don’t fit cleanly into a system.

As more of those situations are handled by systems, fewer employees will have the opportunity to develop that kind of judgment in the first place.

At the same time, many institutions are facing the “silver tsunami,” a wave of Baby Boomer retirements that will have a cross-institutional impact, leaving areas like lending, operations, and risk victims of the “Baby Boomer brain drain.” Decades of tacit knowledge are leaving the building. Not just what people did, but how they thought and how they handled exceptions. That knowledge doesn’t transfer automatically into systems.

This loss of expertise may not become immediately obvious. It will emerge in the fringe cases, when something doesn’t fit the model, when a pattern hasn’t been seen before, or when the system doesn’t have a clear answer. In those moments, the question isn’t whether the system works, it’s whether anyone inside the institution still knows how to operate without it.

To protect institutional knowledge, be intentional about:

- Ensuring employees still encounter and work through situations that fall outside standard workflows

- Capturing how experienced staff handle exceptions and edge cases before that knowledge leaves the organization

- Maintaining the ability to operate when the system doesn’t have the answer

3. The Experience Misalignment

AI will continue to improve the efficiency of customer interactions. That part is already happening. Chatbots, virtual assistants, and AI-enhanced service tools will handle more routine inquiries, faster and more consistently than before. For transactional interactions, that’s a clear win.

But in financial services not all interactions are transactional.

Some of the most important moments like fraud disputes, credit denials, and customers experiencing financial hardship are highly emotional and situational. These aren’t just requests for information, they’re moments where context, judgment, and empathy matter.

Across industries, there are already early signals. Automation improves speed and containment, but satisfaction drops when customers can’t easily reach a human in more complex situations.

That creates a potential misalignment, as institutions will optimize for speed, containment, and cost while customers will evaluate the experience based on clarity, resolution, and trust. Those two things don’t always line up.

The result won’t necessarily be failure. It will be something harder to detect. Interactions that technically work, but still feel a little off or experiences that are efficient, but not quite reassuring. For community institutions, that distinction matters more than it might for larger players, because relationships are a big part of their value proposition.

To maintain strong experience levels, be intentional about:

- Defining where human interaction still matters most and protecting those moments

- Making it easy for customers to move from AI to a person when the situation calls for it

- Paying attention to how interactions “feel,” not just how efficiently they’re handled

So What?

AI isn’t introducing entirely new challenges to banking. It’s accelerating ones that have always been there: system dependency, knowledge transfer, and customer experience tradeoffs.

None of these will show up as immediate problems. In most cases, early results will look positive: faster workflows, cleaner outputs, better metrics. That’s what makes them blind spots. They don’t show up when things are breaking, they show up when things are working and we aren’t paying attention.

For banks and credit unions, the opportunity isn’t just to adopt AI. It’s to do it with a clear understanding of what might change along the way. Because the institutions that get the most out of AI won’t just be the ones that move first. They’ll be the ones that see these patterns early, while there’s still time to do something about them.

Tristan Green is a director at Cornerstone Advisors. Follow Tristan on LinkedIn.