A very real reason to explore strategies that can offset the impact of the coronavirus

The coronavirus continues to evolve and make things more and more challenging for payments professionals. In this article, I present my projection for the impact of the pandemic on interchange to the average financial institution based on three different economic scenarios.

My model is based on five key assumptions:

- The projection is based on 10,000 accounts.

- While overall GDP shrinks based on the numbers above, I assumed much of the transaction volume does not disappear but instead migrates to different merchant types (e.g., more digital commerce and less travel).

- As debit volume migrates to more grocery, I adjusted the mix of PIN and signature transactions and took the interchange rate down accordingly.

- Interchange growth is typically slightly higher than GDP growth (5% to 6% is the benchmark), so I think the reduction would also be somewhat less than GDP.

- These assumptions are against a flat baseline.

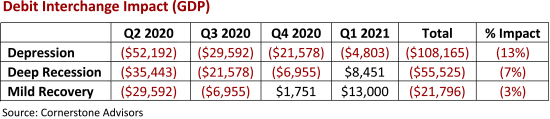

Based on the migration of transactions to different types, overall reductions in spend, and a slightly less severe impact than the overall GDP impacts, here are my projected impacts:

The range of outcomes is a reduction of 3% to 13% in interchange income not including growth. So, the average institution with 50,000 accounts could expect an interchange revenue reduction of between $100K and $500K over the next year. Institutions that have a baseline growth of 5% to 6% built into their forecasts could be looking at double or triple the impact.

These numbers illustrate how it is more critical than ever for financial institutions to look for opportunities to leverage existing resources to execute against these key payments initiatives and minimize the impact to their businesses. Read more on this topic in Payments in the Pandemic: Five Ways Financial Institutions Can Make a Difference Today.