Consumer remote deposit capture has begun to turn heads as technology stumbling blocks are slowly being lifted and banks and credit unions look for new ways to grow deposits and cut costs. Thanks to Federal Financial Institutions Examination Council guidance released earlier this year, financial institutions finally understand where the regulators stand. Although today installations are mostly limited to a few niche institutions, there may be some light at the end of the tunnel for more mainstream adoption. Timing, however, is critical as check volumes continue to decline.

This article looks at the history of CRDC, provides an overview of the latest regulatory guidelines, and presents some best practices banks and credit unions can use when thinking about deploying a solution.

This article looks at the history of CRDC, provides an overview of the latest regulatory guidelines, and presents some best practices banks and credit unions can use when thinking about deploying a solution.

PART I: HISTORY

It’s been almost five years since the Check Clearing for the 21st Century Act (Check 21) was introduced. Since then, many financial institutions have taken advantage of the legislation by deploying remote deposit capture solutions, including branch/teller capture, that have cut courier costs and float times. Also, merchant capture solutions are now widely installed and have been very successful. Many banks and credit unions, noticing this success, are taking a harder look at offering remote capture to their consumers.

At first glance, allowing consumers to scan checks from home is a “no-brainer”. It’s easy, convenient, cheap and tech savvy! So, why hasn’t there been more adoption?

At first glance, allowing consumers to scan checks from home is a “no-brainer”. It’s easy, convenient, cheap and tech savvy! So, why hasn’t there been more adoption?

The biggest obstacle in the past has been the technology available to the consumer. Notably, consumers didn’t have a way to scan their checks. Today, many printers come with a built-in scanner. With the latest applications, any desktop scanner works.

In fact, there have been a few success stories to talk about. Notably, the pioneer in consumer capture was USAA. With military personnel scattered throughout the world, USAA needed a better way to gather deposits. In 2006, it rolled out Deposit@Home, where any desktop scanner would integrate with the association’s online banking site and checks could be captured electronically. As a member, I took it upon myself to give it a try to see if it was as easy as the Web page claimed. I was very surprised how well it worked. Within seven minutes I logged into online banking, signed up for Deposit@Home, installed the java applet, scanned the check and had the money in my account. There were no errors with my scanner, no check holds…very nice!

Last year, corporate credit union EasCorp introduced its DeposZip product. While this product is not as integrated as USAA’s, it gives credit unions a quick entrée into consumer capture. On the bank side, not much has transpired. First Command Bank, which offers military families all over the world banking services and competes with USAA, last year introduced Deposits On Command, allowing customers to scan their checks.

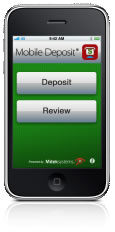

Recently, new technology was developed that allows mobile phone cameras to act as scanners. A good example of this is Mitek’s ImageNet Mobile Deposit product. Another breakthrough from USAA was announced last month regarding the release of its RDC iPhone product, where the iPhone would work as a scanner. Pretty cool stuff.

Recently, new technology was developed that allows mobile phone cameras to act as scanners. A good example of this is Mitek’s ImageNet Mobile Deposit product. Another breakthrough from USAA was announced last month regarding the release of its RDC iPhone product, where the iPhone would work as a scanner. Pretty cool stuff.

PART II: THE REGULATORS

In January of this year, the FFIEC issued Risk Management of Remote Deposit Capture, which provides guidance regarding the use of RDC including merchant, branch, teller, ATM or consumer capture. The guidance was long overdue as banks have been deploying this technology since the introduction of Check 21.

As with the announcement of any new system, all prior FFIEC guidelines regarding vendor management are discussed. This includes performing proper vendor due diligence, performing a detailed needs analysis and measuring and monitoring the vendor. (See some past articles: Manage That Vendor! and Take a Free Vendor Management Aptitude Test)

The FFIEC makes it very clear that this is not merely a new service but a new delivery system, and risks should be assessed accordingly. It actually goes into pretty good detail on some of the risks associated with RDC. Here are a few of examples that are related to consumer capture:

Legal and Compliance Risks

-

Because checks are legal documents, having proper controls in place that are consistent with regulations regarding the capture and exchange of i/wp-content/uploads// is very important.

-

Timing should be evaluated for holds, settlements, exceptions, etc. to verify they meet regulations and agreements in place.

-

Remote capture raises the risk of money laundering. FIs need to understand potential risks and mitigate them.

Operational Risks

Operational Risks

-

As with any technology vendor, safeguarding customer information is very important. Due to the sensitive nature of information involved with RDC, management needs to assess and mitigate any risks associated with securing non-public customer information.

-

Second only to technology, fraud is a key reason for the lack of consumer capture deployments today. There are several instances where fraud can take place. The simplest example is where a customer deposits a check using your RDC solution then, instead of destroying the item, deposits it at another institution. Also, built-in security features on checks may be lost when capturing checks electronically. Counterfeit checks are also much harder to detect in a remote capture environment. The FFIEC is concerned that these and other fraud risks are clearly understood and should factor into the overall risk mitigation efforts by your institution.

PART III: DEPLOYMENT BEST PRACTICES

1. Identify the number of potential users

The first order of business is to butter up the marketing/IT data geek at your institution. He or she will prove to be quite handy as you begin to segment your client base. It may be something as simple as pretending to be interested in the success of a current marketing campaign. If it’s an IT person, get them the latest PS3 game. They’ll be a friend for life.

Once you have the data guru’s attention, come up with some filter criteria. You’ll want to fool around with some queries like these:

-

Active Internet banking users

-

Customers living more than 10 miles from the closest branch

-

Businesses that don’t use merchant capture

-

High net worth customers

-

High volume check users that don’t use merchant capture

2. Determine Criteria for enrollment

Don’t let the data head go just yet. Once the potential users are identified it will be important to qualify the base. The qualification should look at the customer’s history with your institution. Some criteria to review include account longevity, credit score, NSF history, average balance, etc. Limits and holds should be set based upon these criteria.

3. Design a service that’s integrated and user-friendly

If you’re comfortable with the number of potential users identified above, then it’s time to implement a solution. The first rule of thumb is to always keep the customer in mind when designing a service. Think about these things:

-

Choose an integrated/easy to use solution. Customers want a single look/feel when going online – if it’s not the same look/feel, make sure it’s at least a single sign-on. Further, customers want an easy to use application that is error-free and works with any browser. Be wary of applications that require software to be installed as firewalls/browser security can cause roadblocks. The Java applet that USAA requires didn’t seem to give me any trouble.

Choose an integrated/easy to use solution. Customers want a single look/feel when going online – if it’s not the same look/feel, make sure it’s at least a single sign-on. Further, customers want an easy to use application that is error-free and works with any browser. Be wary of applications that require software to be installed as firewalls/browser security can cause roadblocks. The Java applet that USAA requires didn’t seem to give me any trouble. -

Automate as much as possible. Human intervention leads to inefficient processes and potential errors. You will never get away from working exceptions, but establishing risk-based limits and automated interfaces to/from core systems should be the goal.

-

Don’t overspend. It’s no secret that check volumes are going to continue to decline. The payoff of a large custom deployment will be hard to justify even at current volumes.

Conclusion

Consumer RDC continues to gain traction but its future is unknown. When you dig under the covers, it begins to make some sense, especially as the technology matures. The product’s “stickiness” alone makes it worth a look. It’s hard to predict whether this will be a product that caters to a few niche institutions or become commonplace in traditional banks and credit unions across the country. It’s clear that customers who use RDC, whether it’s business or personal, get “hooked” on the convenience. As regulatory guidelines become clearer and technology catches up, it gives banks and credit unions a low-cost way to gather deposits and helps create loyal customers. It’s a race between technology innovation and declining check volumes. The winner is yet to be determined.

-ew

Smart Technology Solutions

From evaluating the adequacy and associated risks of your technology environment, to choosing a vendor solution, to negotiating a contract, to managing the conversion – Cornerstone Advisors offers a full host of services to help you survive the challenges presented by an ever-changing marketplace.

Visit our Web site or contact us to learn more about our Technology and Risk Management services.